Economic Reports

NOVEMBER 2021

So the FED announced the beginning of tapering. Why you should care..

At the November meeting of the Federal Open Market Committee (FOMC), the Fed announced the anticipated beginning of tapering. To ease economic stress brought on by the temporary closing of businesses and other far-reaching measures in reaction to the COVID-19 pandemic, the Federal Reserve began to buy an increased amount of U.S. Treasury bonds and mortgage-backed securities. These acts help keep interest rates low and provide liquidity to an economy thrown into chaos. Tapering is the gradual process of unwinding the strategy over time.

The Federal Reserve has adequately foreshadowed this move so as to not cause disruption in credit markets and the economy as a whole. The announced plan is to pare back $15 billion in purchases per month ($10 billion of U.S. Treasuries and $5 billion in mortgage-backed securities) for the months of November and December 2021. The plan after December is explained in the Committee’s statement as follows “the committee judges that similar reductions in the pace of net asset purchases will likely be appropriate each month, but it is prepared to adjust the pace of purchases if warranted by changes in the economic outlook.”

Being “prepared to adjust the pace of purchases if warranted” is related to the Committee’s employment target balanced against its inflation target. An accommodating interest rate strategy aids higher employment. But, that risks inflation rising beyond the current target of 2% annually.

First, let’s look at employment. Today’s jobs report came in at 531,000 new jobs created. This exceeded expectations, which was in the 460,000, range by a nice margin. Many excited headlines claimed that this was the economy returning to normal. Although, it comes on the heels of two consecutive months of wide misses. We choose the more realistic reaction of being cautiously optimistic.

On the inflation issue, The Fed’s target has long been 2% annually. After years of inflation below 2%, it appears that the Fed has become flexible. They have alluded to a 2.6% inflation rate in the short term to balance out the years below their target. Further, it is their position that inflation currently is a supply-side issue related to disruptions in the supply chain.

We accept that current inflation is transitory. But, we are moving from one transitory event to another. The next expected cause of inflation will come from wage inflation. We already see increasing labor costs. Tie that with the recent unemployment report, and you can expect wage inflation. To us, this implies overall inflation lasting longer than the Fed appears comfortable admitting.

All indications point to an increase in interest rates in the second half of 2022. We hear that half of the Committee wants to raise rates now. The FOMC left rates at the current level of 0-0.25%. This is the rate target of the Fed. We already see yields to maturity increasing in the secondary market; 2 basis points in the 20 year Treasury and 3 bps in the 30 year Treasury. When interest rates go up, the market value of existing bonds goes down.

All of this continues to support our thesis of adding real estate to the investment portfolio as a prudent strategy; a recovering economy, an inflation hedge, and investment yields via rent payments driven by markets rather than bank policies.

OCTOBER 2021

Continued inflation and volatility in the markets?

Fed tapering is set to begin. In response to the COVID-19 related economic shutdown, The Federal Reserve initiated an unprecedented liquidity program that kept interest rates low and supported markets that had severely malfunctioned. The bond purchases put $4 trillion on the Fed’s balance sheet.

Fed Chairman Jerome Powell commented that the “policy will remain accommodative until we have reached” the bank’s targets on unemployment and inflation. It is expected that the Fed will unwind this program by mid-2022. We can derive from this that the Fed foresees the economy to reach its unemployment target in this time frame.

In previous reports, we have alluded to the divide among the Fed’s board members on interest rates. Half of the Board is pushing for an increase in interest rates to fight inflation, while the other half is obligated to hold rates low until economic goals are met. The group has raised its inflation expectation for the next year from 3.0% to 3.7%. That sizable jump reflects the understanding that the current supply chain bottlenecks causing inventory shortages will last longer than previously anticipated. Since we last reported on the forty vessels anchored off of the Long Beach and Los Angeles shores, the number has swollen to seventy-seven ships.

Year over year CPI (Consumer Price Index) rose 5.3%. This number is much higher than we have been accustomed to in the past few decades. Real estate and commodities have historically been held as hedges against inflation. Commodities do tend to respond quicker in price. They also have carried greater downside risk. Real estate tends to be less volatile and is designed to produce income while you wait for the value to increase.

September’s jobs report missed expectations by a wide margin, with only 194,000 jobs created. The consensus expectation was 500,000 growth for nonfarm payroll. This is now two months in a row that the jobs report has been weak, and analysts have wildly missed the mark. If we look a little deeper, we find that private-sector jobs came in at 317,000. A 123,000 decline in government payrolls offset this. Even with 317,000 jobs created in the private sector, that’s still a notable miss of the 500,000 expectation. The majority of private-sector jobs are in the hospitality and leisure sectors. This could well be restaurants, and travel accommodations are reopening from the COVID shutdown. This weak number may slow the Fed’s tapering and expected rate increases.

Stock and bond markets have experienced high volatility over the past month. Stocks have flip-flopped to extremes from one day to the next a few times. September has historically been a highly volatile month. More of the same in October would not surprise us.

Again, we reiterate that asset allocation using non-correlated assets like real estate can soften the extreme swings in a portfolio.

We are intentionally not commenting on the political drama of the U.S. debt ceiling battle. The two political parties will play out the drama as they always do, each wrangling for power in Washington. If their work impacts our outlook on real estate investing, we will discuss it here.

SEPTEMBER 2021

The Delta variant, supply chain disruption, and Federal Reserve tapering leading the way of economic impact.

Will Delta upend the economy? This report will dive into the details and look at how real estate is a defense move in uncertain economic and market times.

The August jobs report disappointed. The expectation was 720,000 new jobs, but came in at a disappointing 235,000. The COVID-19 Delta variant appears to have caused a slowing in hiring as employers have concerns over restrictions to conducting business and employees have concerns over returning to work.

Unemployment fell to 5.2% for August, down from July’s 5.4%. It is essential to understand that the unemployment number includes only those workers actually looking for work. With current conditions, people choosing not to enter the workforce right now is not a surprise. As per the bureau of labor statistics, the current workforce participation rate is 61.7%, unchanged from a year ago. But substantially below the norm.

The University of Michigan Index of Consumer Sentiment and Index of Consumer Expectation are both sharply lower month over month. The consumer sentiment index fell 13.4 points and the consumer expectation index fell 17.6% from July to August. The indices are down 5.1 points and 5.0 points respectively compared to August 2020. The Conference Board’s Consumer Confidence Survey is sharply lower by 11.3 points at 113.8.

The supply chain is currently bottlenecked. Many products and materials are slow to reach their destination. There are now a record number of cargo ships waiting to unload at the Long Beach and Los Angeles ports. According to the Marine Exchange of Southern California, there are 44 ships anchored. Typically, there are none or one waiting, according to Kip Loutitt, executive director of Marine Exchange. Transport from Shanghai to Chicago has gone from 35 days to 73 days.

One example of problems shows up in the auto industry where new car supplies are limited because of the slow delivery of microchips. Supply and demand have just about eliminated negotiations in auto purchases. Consumers take just whatever they can get pushing the average new car purchase price to a record $41,000. This has rippled into the used car market with a record average purchase price of $25,000. It is just one example of how supply chain disruption causes increasing prices.

The Delta variant and supply chain complications are forefront with the Federal Reserve. At the last minute, the Kansas City Federal Reserve annual convention was switched from in-person to virtual. Chairman Powell continued his position that current inflation will work itself out. But, it appears that the Fed’s outlook on this has moved from a few months to a year or more.

The Fed remains committed to begin tapering in Q4 2021. Tapering is the process of gradually reducing the amount of bonds being purchased to provide liquidity and to hold interest rates down. We have heard reports that the committee is divided on the path forward. One side questions continuing to

provide liquidity because of the inflation risk of doing so when goods are not available but money is, and the other side wants to remain committed until the unemployment and economic targets are hit. Chairman Powell will have a balancing act to keep both sides happy.

Supply bottlenecks, Delta and labor issues are all hitting the construction market as well. New home supply is now about half what it was two years ago. According to Redfin, a real estate firm based in Seattle with offices nationwide, over half of all homes are selling above the listing price, 55.5% versus 30% one year ago.

This situation puts upward pressure on home prices, which benefits investors in multi-family apartment buildings. As home prices have gone up, so has rent at a time when vacancies are going down. The chart below from Apartment List shows the rapid increase in average rent and the potential income to be made by real estate investors.

Image credit: Bloomberg

The White House economic policy may suffer distraction from the rather complex geopolitical situation of Afghanistan. We do not know yet if this distraction will have an impact. But, we do know that people are taking a more defensive position with investments by moving into healthcare and real estate. The Dow Jones U.S. Real Estate Index has had a sharp uptick since August 26, gaining over 3.5% in just a little over one week. We reiterate that real estate has historically been a hedge against inflation.

AUGUST 2021

The Federal Reserve’s Federal Open Market Committee held its regular meeting with no surprises. The committee voted unanimously to hold interest at the current level, a 0-0.25% range. In their official statement, the FOMC discussed economic activity that has continued to strengthen but is not yet to the level they would call “fully recovered.” The statement was more pointed on the Fed’s goals of maximum employment and inflation control. They did, however, drop the word “substantial” to describe the expected “progress.” Their sentence reads, “…the economy has made progress toward these goals, and the Committee will continue to assess progress in coming meetings.”1

The statement covered the committee’s standing position that inflation has remained below the Fed’s long-term target of 2%. This may cause our readers to be a bit surprised as we have seen rapid inflation recently. The committee continues to hold the position that recent inflation has been caused by bottlenecks in the supply chain that will wash out as time goes by.

For readers not familiar, the activities of the Federal Reserve indirectly impact the commercial real estate sector in several ways. From impacting interest rates to facilitating or slowing the economy. Commercial lenders follow the lead of the Federal Reserve, and the Fed’s setting of interest rates can spark economic growth or slow the economy to restrain rising inflation trends.

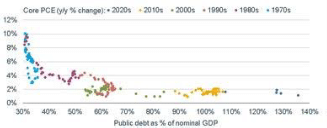

We cannot look away from increased government spending, though, as it relates to the perception of the possibility that such spending risks increases of inflation. However, the chart below goes against this logic as it shows federal debt growth has expanded, yet inflation moved lower. We attribute this to increased amounts of U.S. Treasuries being purchased by foreign buyers. This helps keep the cost of servicing U.S. debt low. This chart covers every decade since the 1970s and the relationship between GDP and PCE (Personal Consumption Expenditures). Should foreign buyers find suitable alternatives, we can expect rising interest rates.

Image credit: Bloomberg

There was no reference to the COVID-19 Delta variant in the FOMC statement. We are all well aware of the disruption that COVID-19 has caused, and we can expect that a widespread Delta or subsequent variant will cause an economic disruption. However, we believe that, simply through experience and lessons learned, such a disruption would be better managed than the initial complications of 2020. We do not believe that the committee thinks that COVID-19’s impact is minimalized. The statement left out the June phrase of vaccines having “reduced the spread of COVID-19 in the United States.” We conclude that the committee remains concerned about the original virus and variants.

The FOMC has been purchasing $80 Billion in U.S. Treasury securities monthly since September 2020 and $40 Billion in mortgage-backed securities monthly in that same time frame. In the July meeting, they committed to continuing at that same pace of $120 Billion per month. Chairman Powell has stated that tapering will occur with substantial advance warning.

With the current FOMC position, we are led to believe that rate increases would not likely occur until late in 2022. We are not predicting this, and, of course, we have no crystal ball. But tapering, we expect, would take about six months. The Fed has confirmed that they will stand pat for the foreseeable future and that they will provide a substantial warning. When adding commercial real estate to your asset mix, doing so in a low-interest-rate environment is opportunistic.

JULY 2021

The International Monetary Fund raised its outlook for the 2021 U.S. economy to the highest in a generation. The 7% growth outlook was bumped up remarkably from the previous 4.6% forecast issued as recently as April. This dramatic revision is based on the expectation that both the American Jobs Plan and American Families Plan will pass Congress. The IMF must be confident to have released their report.

The Congressional Budget Office has estimated that 2021 economic growth will amount to 6.7%, the fastest calendar-year expansion since 1984. We will have details in next month’s report.

Consumer confidence rose in June almost back to its pre-pandemic level, according to the Conference Board. The percentage of American consumers who plan to buy a home, car or major appliance appear to move ahead even with rising prices. Home prices shot up in April by the most in 15 years.

The S&P 5001, after setting new record highs for several consecutive days, closed June up 93.39 over May at 4297.50. The higher the market goes the greater the risk that it will decline. We say proceed with caution and use real estate as a diversifier to mitigate stock market volatility.

The biggest challenge in the economy right now is finding workers willing to return to work. The service sector; hotels, retail, restaurants, casinos, etc., is having the biggest challenge. In June, 6% of workers quit in this sector. That’s twice other industries. Competition to attract workers has increased. Jobs board, Indeed, report that job postings offering a signing bonus have doubled.

Randstad North America’s chief executive, Karen Fichuk, says that job postings were up 40% in June while employment searches were up only 4% on their jobs board Monster. Randstad is a staffing and recruiting firm.

Analysts expect that 675,000 new jobs were added to the economy in June. That government report is expected tomorrow, and we will have a recap in next month’s report. Factory output has been expanding at an accelerated pace. Companies are investing more in capital goods and technology.

It appears that our monthly report would not be complete without our theme of recent months, inflation. Yes, here we are again discussing inflation. And we are again suggesting that you look at commercial real estate as an inflation hedge.

First, the FOMC at their June meeting discussed that inflation is beyond their target level. But, still hold to the idea that it is temporary. Next, we have to look at reality. Inflation made its most significant jump since records have been kept. Now, consider the two large spending plans cited above and the IMF’s reported outlook. With an equation like this, it is highly possible that more inflation is to come. The FOMC did hint at talking about raising interest rates in the future.

JUNE 2021

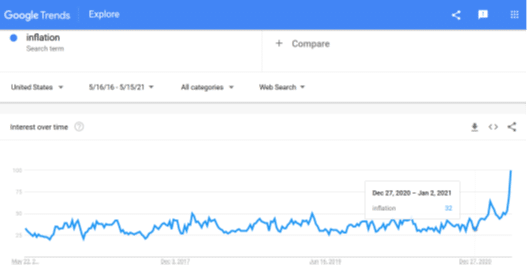

At first, it may seem like an odd combination. We’ll explain. We’ve talked about inflation in each of our economic reports. It seems that almost everyone is becoming interested in the topic now. By June, the internet searches via Google with the word inflation reached an all-time high for the search engine. Google Trends is a way to gauge people’s interest in a topic compared to other time frames. A score of 100 shows the highest interest relative to other times. Compare that to a relative score of 32 as we entered 2021.

Inflation is a significant factor relative to commercial real estate investing; construction material inflation makes new buildings more costly, causing existing buildings’ values to trail upward right behind new buildings increased cost. In addition, people get used to higher prices and are more willing to accept them. Owners of real estate benefit accordingly. Inflation adds to capital appreciation, and owning real estate serves as a hedge against inflation in other areas of your financial life.

The current inflation surge may have slowed, but we expect continued inflation at a higher than average pace. The recent rise in inflation was caused partly by a clog in international shipping routes. This has caused an increase in shipping costs and a supply/demand imbalance. There are signs of easing. Currently, 20 ships are waiting to unload at Los Angeles and Long Beach. At the peak in Q1, there were 40. The Baltic Dry Goods Index, an index of raw material like iron ore used to make steel for commercial real estate construction, has begun to ease as well. It moved from 500 last summer to 3,250 in early May and now has pulled back around 2,800.

We see a continued risk of inflation coming from two areas; more government spending and signs of solid economic growth potential. The two usually do not coexist. Government spending is usually a short-term

remedy for the absence of economic activity. We’re not here to take political sides. We are here to convey what we see so you can be better informed and profit thereby.

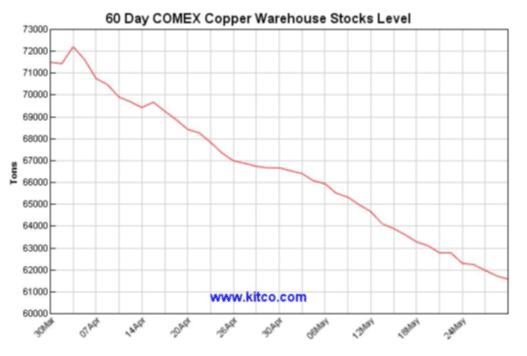

This is where Dr. Copper comes into the picture. Copper is said to have a Ph.D. in leading economic indicating. It is a metal widely used in manufacturing and construction. The chart below shows a continued increasing trajectory in the copper spot price, indicating that manufacturers believe that they can still earn a profit while paying higher prices for raw materials.

Further evidence of manufacturer confidence that copper offers is found in current warehouse supplies. Over the past couple of months, manufacturers have been buying copper faster than it can be produced. We believe this indicates confidence by manufacturers of continuing solid economic activity.

The primary rule of real estate, location, notwithstanding, we believe the current conditions point to an attractive time to invest in commercial real estate. Let’s clarify this a little. Anytime is a good time to invest in commercial real estate for long-term investors and those who need to diversify their overall portfolio with an alternative or non-correlated assets. To clarify further, we believe the current conditions offer an even more attractive timing.

The timing to use real estate as a hedge against inflation is upon us as President Biden has proposed a massive $6 Trillion budget for FY2022 following trillions of economic stimulus money added to the economy over the past year. With the indicators showing confidence in future economic growth, it is easy to conclude that there will be greater demand for commercial square footage. Skyrocketing home prices and short supply leaves hopeful home buyers remaining in multifamily complexes, an opportunity for savvy real estate investors.

MAY 2021

The American Families Plan legislation is one of the recent government spending programs floating around Washington. The plan emphasizes President Biden’s promise to raise taxes. One point of concern is an increase in capital gains taxes. Tax increases have historically led to a higher interest in commercial real estate investing because of the tax shelter features of such an investment.

Congress will work out the details of just what the tax increases will be. Once done, it is likely that the increases will pass along party lines, even the current thin margin. It is expected that wealthier households will be hit with higher capital gains taxes making our work even more impactful in serving our investors. It is not our desire to be involved in the political debate. But, we desire to do the best we can for our investors regardless of what the debate in Congress may yield.

Commercial real estate investing holds the potential for deferring capital gains taxes through the use of a 1031 exchange, named for the section where it is found in the tax code.

The FOMC, Federal Open Market Committee, held its meeting in April. As expected, interest rate targets were not changed. FOMC believes that more recovery is needed before the action should be taken. We listened to Federal Reserve Chairman Jerome Powell’s news conference as he laid out the Fed’s view on inflation. The target remains at 2% annual inflation. Chairman Powell expects, though, that short term inflation to rise above 3% as the economy restarts after the structured shutdown related to the COVID pandemic. Though 915,000 jobs were added in March, Mr. Powell pointed out that we are still more than eight million jobs fewer than we were a year ago.

Later that same day we listened to President Biden announce his spending plans which could top $4 Trillion. The aggressive government spending proposals have most inflation hawks nervous. There is always the risk that the Fed may not get out in front of inflation caused by so much cash hitting the economy artificially. Real estate has, historically, been a hedge against inflation.

The cost of construction material has risen sharply in just the past few months. According to KGW8 in Portland, Oregon lumber costs have quadrupled in the past year. This will have an indirect impact on the value of existing structures as investors will be more attracted to the values in existing properties.

GDP came in at a very attractive 6.4% for Q1 2021, consumer confidence is up, the Chicago Fed National Activity Index (CFNAI) is up, small business lending is up, building permits are up and interest rates are down. Below is our chart of economic indicators for your review.

APRIL 2021

The American Rescue Plan Act of 2021, a $1.9 Trillion government spending plan, has been signed into law. It comes on the heels of Trillions in government spending in 2020. The Biden Administration has alluded to an additional $4 Trillion in government spending.1 We will not endeavor to predict what this may mean for future inflation. But anyone who has taken an Economics 101 class understands that excess money added to an economy has the potential to spark inflation sometime in the future.

As it does with any hard asset, commercial real estate can serve as a hedge against inflation for investors who hold the investment—all the more reason to get in early.

Inflation is a result of more money chasing fewer goods. To slow the economy so that it does not overheat and lead to a sudden collapse, the monetary and fiscal policy is adjusted to slow things down. One result is an increase in interest rates. The return on investment (ROI) that real estate investors may realize has a more significant opportunity when rates are low like they are now compared to historical averages. Again, a reason to invest before interest rates are pushed up.

With any new administration in the White House, a concern for Americans is always the tax policy of that new administration. There has been much speculation that the Biden administration will push for tax increases, especially on top income earners. President Biden has alluded to such in recent public statements.

We believe that tax increases can make investments in commercial real estate even more attractive from a tax planning strategic view than other asset classes that do not enjoy the tax benefits of real estate. This condition has the potential to push more investors into this investment space. With an increase in buyers over sellers, real estate values would be expected to go up. They are, again, benefiting the early investor.

The Washington Post has reported that the Biden Administration will push for $3 Trillion in tax hikes.1 We believe that the same people who qualify as Accredited Investors for private placement purposes will be the top taxpayer profiles to be the target of increased taxes. We endeavor to stay out of the partisanship of this topic and remain focused on how it may impact our commercial real estate investors.

The stock market continues to hit new record highs in all three major indices. The Dow Jones 30 hit new records 17 times so far in 2021, and its most recent record was just March 29. Hitting record highs is not a sign among professional managers that the market will be caused to go higher. In reality, the higher the market goes, the greater likelihood of risk that it will reverse course. This shouldn’t be as big a concern for investors who add non-correlated assets like real estate to their portfolio.

The current economic and market conditions reinforce our belief in investing in commercial real estate. As always, we welcome your questions about your existing or potential CRE investments.

Newsletter

Useful links

CONTACT

- BLOOMFIELD HILLS, MI

- +1 (802) 222-0364

- contact@handsoffinvestment.com

Disclosure of Interests:

Nothing on this website is intended to provide tax, legal, or investment advice. You should consult your business advisor, attorney, or tax and accounting advisor regarding your specific business, legal or tax situation. All pictures shown in this document are for illustration purpose to show the type of properties that HANDS-OFF INVESTMENT invests into and are not current offerings.

No Offer of Securities:

Under no circumstances should any material on this site be used or considered as an offer to sell or a solicitation of any offer to buy an interest in any investment. Any such offer or solicitation will be made only using the Confidential Private Offering Memorandum relating to the particular investment. Access to information about the investments is limited to investors who either qualify as accredited investors within the meaning of the Securities Act of 1933, as amended or those investors who generally are sophisticated in financial matters, such that they are capable of evaluating the merits and risks of prospective investments.

Confidentiality:

Handsoffinvestment.com reserves all copyright and intellectual property rights to the content, information and data within this site. The contents within handsoffinvestment.com may not be modified, reproduced, stored in a retrieval system, transmitted (in any form or by any means) or used in any other way for commercial or public purposes without the prior written consent of handsoffinvestment.com. The recipient agrees to keep the contents of this site confidential and use it solely for personal use.